Cardlytics: Fintech walled garden

Share price: 79USD ($CLDX)

Market Capitalization: 1,95B$

1. Elevator pitch

Cardlytics operates an advertising platform within financial institutions (FIs) digital channels that have access to anonymized purchase data of more than 150M digital banking customers. By leveraging this data Cardlytics can provide targeted advertising in the form of cashback offers that are relevant to the consumer and provide a measurable ROAS to the advertiser.

This is a classic “platform-like” business model that is reinforced by network effects, Cardlytics platform is in its infancy and ARPUS are set to increase with the launch of a shelf serve platform, allowing the company to go after the big tail of advertising.

2. Company Overview

Cardlytics was created in 2008 when two bankers, Scott Grimes, and Lynne M. Laube recognized banks and credit unions were sitting on an untapped well of data. They created a platform that operates inside online banking apps, that shows personalized cashback offers whenever a bank customer logs into his account.

The user experience is super easy and fun, like an online treasure hunt. Whenever a customer logs into his account he´ll see a few little square logos, these little logos are the discount offers based on the customer´s purchase data.

So, let´s say you spend a few hundred dollars on coffee every month, you usually purchase your coffee at Dunking Donuts and you happen to buy your coffee close to a Starbucks Store; then the next time you open your banking app you´ll probably see a 15% cashback offer on your next Starbucks purchase, and if your purchase history shows that you are less loyal to the brand then you´ll probably be offered a 5% cashback offer. If you are interested in the offer you just have to click on the logo, claim the offer, and the next time you use your bank´s credit or debit card to buy at Starbucks(the offers usually expire in a month) you´ll automatically earn cashback into your account.

From the Cardlytics perspective, they get paid marketing dollars by big brands like Starbucks or Airbnb which is reflected in the annual reports as billings; these billings are evenly split between customers, FIs(banks who use the platform), and Cardlytics. From every marketing dollar 1/3 goes to the customer in the form of cashback offers, the remaining 2/3 are labeled as revenue which is split between bank partners and Cardlytics ( their part of the pie is called adjusted contribution which is approximately 50% of the revenue ).

This platform-like business is reinforced by network effects: as Cardlytics grows its number of users (MAUs), more advertisers get attracted to the platform, making the offers more attractive to the consumer which makes more FIs want to partner with Cardlytcis and so on. Cardlytics targeting capabilities get better with an increasing amount of data, making the platform more valuable for both advertisers and consumers.

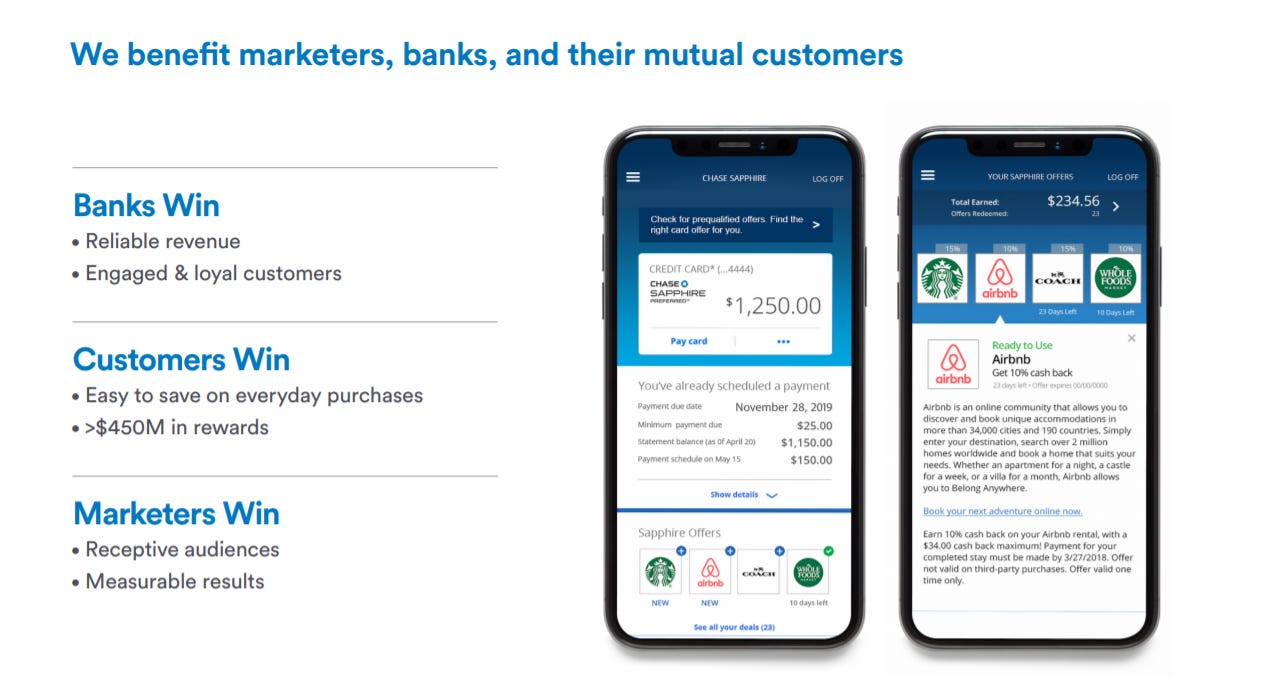

Everyone wins:

Banks win: banks get an extra source of revenue and, given that discounts encourage card usage over cash, they are rewarded with more frequent and loyal users who tend to interact more often with their banking app.

Customers win: customers are offered relevant and targeted discounts based on their previous shopping experiences. The customer finds these rewards compelling (system-wide opt-out rate is less than 0,5%) which is reflected in a 7% click-through rate.

Advertisers win: Cardlytics is the ultimate targeting tool for advertisers who can precisely measure their ROAS (return on advertising spend) by looking at the customer purchasing aggregated data. Every customer in the Cardlytics network is real, data is not shared outside of the platform and the architecture employed to handle a big amount of sensitive information is often cited as best practices.

Cardlytics win: Cardlytics gets a cut of every advertising dollar that is spent on the platform.

Financials

Monthly active users on the platform (FI MAUs) have grown from 44M in 2016 to near 160M in 2020. Due to their scale, Cardlytics oversees 4 out every 5 purchases in the US.

Fueled by an explosion in FI MAUS Cardlytics revenue has increased x3 since 2015 from 77M to 210M USD in 2019, reducing operating losses to approximately 20M; however, ARPU(average revenue per user) hasn’t kept pace with the rapid revenue expansion and it has stalled around 2.3 USD since 2017 before declining to 1.72 in 2019. ARPUs take time to ramp up and implementation differs from bank to bank.

A few years ago the platform was supported by 2.000 regional banks, then in a 2 years’ time frame they signed Chase and Wells Fargo into the platform, and Cardlytics is now used by every major bank in the USA. Nonetheless, this integration and implementation process tends to be tedious and it takes some time before best practices are achieved by every bank partner.

A couple of years ago if you happened to be a BofA customer, you had to click on the deals button to access Cardlytics offers, now these offers are on the front page with the resulting increase in ARPUs( BofA ARPU was 0.2USD at launch and in 2017 this figure was close to 2.3USD ). There are some regional bank partners who are already achieving 4 USD ARPUs.

Covid-19

Before the Covid crisis started, back in 2019, the top 5 marketers represented 27% of revenue; this level of revenue concentration is due to the platform being in its infancy and it’s a hint of what’s to come.

Given revenue is heavily concentrated in the restaurant, retail, and travel categories, it has plummeted 42% in Q2 2020. Cash burn was close to 20M in Q2 2020 but given the strong cash position (100M cash in Q2 2020) and the recent convertible debt raise(200M USD), I think this is a short-term problem that doesn’t impair the value of the company in the long run.

Management

Lynne M. Laube is the cofounder of the company and has served as CEO since 2008, aside from that she has around 30M USD worth of stock (even though their ownership has materially decreased over the years).

Cofounder Scott Grimes and David Evans (former CFO) are retiring from the company. As a replacement Cardlytics has hired Michael Akkerman (coming from Pinterest where he served as a global head of strategic partnerships) and has promoted Andrew Christiansen as the company´s CFO. I think the push towards a self-serve platform will require a different skill set to what it was necessary in the beginnings where former banker Scott Grimes was key in order to cultivate the relationship with the banks.

3. Risks and opportunities

Opportunities

ARPU expansion: this is by far the biggest opportunity for the next 3 to 5 years, Cardlytics customer segmentation and ad targeting are best in class; despite that, there’s still no bidding into the platform and Cardlytics pricing models are in their infancy.

I think this interview provides great insights regarding Cardlytcis attractiveness to the advertisers: https://twitter.com/Lullabitte/status/1312423055973593088

Self-serve platform: In order to realize the huge potential that this represents we must comprehend that right now advertising in Cardlytics is done manually, every advertiser has to set up a team and work hand by hand with Cardlytics in order create relevant ads, but if investing in Facebook has taught me something is that in advertising the long tail matters; Cardlytics is currently working in a shelf serve platform in order to allow smaller businesses to advertise. It is still day one at Cardlytics, every advertising platform that I’m aware of exploded when they built a self-serve platform, being this tool necessary to go after the big tail of advertising.

New categories: this is a platform heavily weighted towards travel, retail, and restaurants and there are currently few verticals; being luxury and e-commerce recent additions. Aside from this, media capabilities are currently very limited. Cardlytics cash-back offers now display a simple logo, but the company is working towards a platform where they could promote individual products (grocery or toothpaste discounts for example).

Tailwinds: more than 70% of U.S. consumer payments are electronic and this percentage is projected to increase in the future, moreover online banking is another trend that benefits the company. According to FIS April saw a 200% jump in new mobile banking registrations while mobile banking traffic rose 85%, so even though the Covid crisis has produced temporary wounds it could lead to long-term benefits. The number of digital banking users in the USA has increased by 20% since 2014 reaching more than 160M in 2019

Reinvestment opportunities: 1/3 of the billings are currently directed towards consumer incentives (the cashback offers), Cardlytcis fully controls this split so either they or their partners can decide to reinvest their revenue share as customer incentives; this has already happened in some campaigns, for example, Chase used part of their revenue share to increase discounts in Airbnb offers from 5% to 15%, resulting in a 67% increase in response rates and average purchase climbing from 440 to 750 USD.

This is understandable given the engagement is trending up, on average bank customers in the channel logged into their mobile banking accounts 7.7 times per month(2016), this metric was 10.27 days per month in Q2 2020.

International expansion: 11% of 2019 revenue was derived from outside the US (mainly the UK), this split has remained fairly constant given their BBVA, Santander, and Lloyds partnerships. There is an opportunity to capture more international revenue given that some bank partners have a big presence in LATAM and Europe.

Risks

Disintermediation: Cardlytcis was created more than 10 years ago and at some point, each of the US big banks tried to build this platform on their own; now Cardlytcis is the only provider in the USA. Advertisers want to buy scale and before securing some big deals (like Chase), they had a hard time trying to reach out to big companies that didn’t see in Cardlytics a big enough channel where to spend both time and money. Although purchase data from a single FI can helpful, aggregated data across the country holds much more value; moreover, banks lack know-how and expertise in order to build and operate a platform like this.

Let’s still say that Chase tries to build the platform by themselves, they are going to see how engagement in other banking apps is higher because customers are offered better and more targeted offers; moreover, advertisers would favor Cardlytcis over Chase given that Cardlytcis has a higher base of users with better targeting and higher monetization rates.

Neobanks: US neobanks have reached an incredible scale in a short period of time by providing a better service. The industry is set for disruption, and even though Cardlytics could offer its platform to the new entrants I doubt this will be the case in the near future given its bonds with the incumbent players.

The following sentence reflects the position of the company about this issue:

"What we do not focus on are kind of alternatives to banks versus we're partners with the banks to help them go protect their customers and help them go protect the digital relationship they have with their customers"

Given the industry-changing landscape and Cardlytics ties with the incumbents, I think this is the biggest risk in the near future.

Cardlytics does not control the user engagement in its platform and given that it acts as a loyalty program to their banking partners if incumbents get displaced Cardlytics will face the same destiny.

Companies like square are trying to aggregate compelling features like tax prep services( Credit Karma acquisition) and investing to become a one-stop-shop for customers. On top of that incumbent banks face disruption coming from tech companies like Google (recent Google Pay launch) who also has compelling cashback offers or Facebook who is about to launch Whatsapp payments.

Bank concentration: bank concentration is very high with the 3 biggest US banks agglutinating close to 50% Cardlytcis MAUS, this could lead to more favorable agreements on take rates which could hinder Cardlytcis revenues.

4. Valuation

Given the recent US Bank launch and the Wells Fargo adoption, on top of online banking tailwinds; I think Cardlytics can get to 200M MAUs in the near future.

Management has stated that at maturity they can sustain 20-25% EBITDA margins, so If we assume 4 USD ARPUs ( some banks are already achieving this number ) at 200M MAUs we would get to 800MUSD revenue which at a 15 to 20% net margins can get us to 120-160M owner earnings, this number lies against a current market cap of 1.95B resulting into a 12 to 16 times owner earnings multiple, which seems inexpensive for a high-quality company with such good prospects.

In the long run, Cardlytics could increase ARPUs and expand their international user base which could lead to a much bigger company; there´s still a lot of execution ahead for this thesis to play out, industry disruption and bank concentration area real issues but the opportunities that lie ahead are exciting.